Executive Summary

To recover from an affordable housing crisis that has been decades in the making, Massachusetts needs Gateway City housing markets to produce new homes in line with increasing demand. These inclusive urban communities must also build new housing in a manner that fosters mixed-income neighborhoods to help Massachusetts close the growing economic divide. While the residents and leaders of Gateway Cities welcome this twofold challenge, the real estate markets in these areas vary considerably in their ability to produce homes for people of all incomes. State and local leaders need information to tailor housing strategies to the reality in each of these markets.

The Gateway Cities Housing Monitor is a new tool to provide the data needed to make effective housing policy decisions. It tracks housing market conditions in the 26 Gateway Cities and their suburbs by asking and answering five critical questions on an annual basis:

- To what extent is Gateway City housing supply keeping pace with demand?

- How affordable is housing for Gateway City residents?

- How do the economics of housing production vary across Gateway Cities?

- Are Gateway City neighborhoods revitalizing?

- Is neighborhood revitalization occurring in an equitable manner?

Each year, the Housing Monitor will also include a special analysis section with an in-depth look at a topic of interest. For this inaugural edition, the focus is on the current housing shortage. We estimated the scale of the current housing supply shortage in Gateway Cities and their suburbs, and the number of new homes that Gateway Cities will need to produce over the next 10 years to stabilize prices and balance supply and demand.

The stories these data tell are nuanced and varied, but in essence they show that Gateway Cities must double the pace of housing production to build their way out of the current shortage and keep up with increasing demand. While the present lack of inventory creates significant housing cost burdens and puts homeownership out of reach for many Gateway City residents, housing market trends over the past decade reflect generally positive developments:

- Concentrated poverty is falling.

- Residents are more stably housed.

- Vacant and blighted housing is returning to productive use.

- Homeownership rates are rising for residents of color.

- Property is appreciating at a faster pace in neighborhoods of color than in majority-White neighborhoods.

Section by section, this Executive Summary fleshes out these key findings in greater detail. It also provides a synopsis of potential goals and strategic action items indicated by this rich analysis of Gateway City housing markets.

Special Analysis: The Gateway City Housing Shortage

This section estimates the number of homes that Gateway Cities will need to produce over the next 10 years to address the current shortage while also keeping up with modest household growth and replacing the older housing stock that is invariably lost each year.

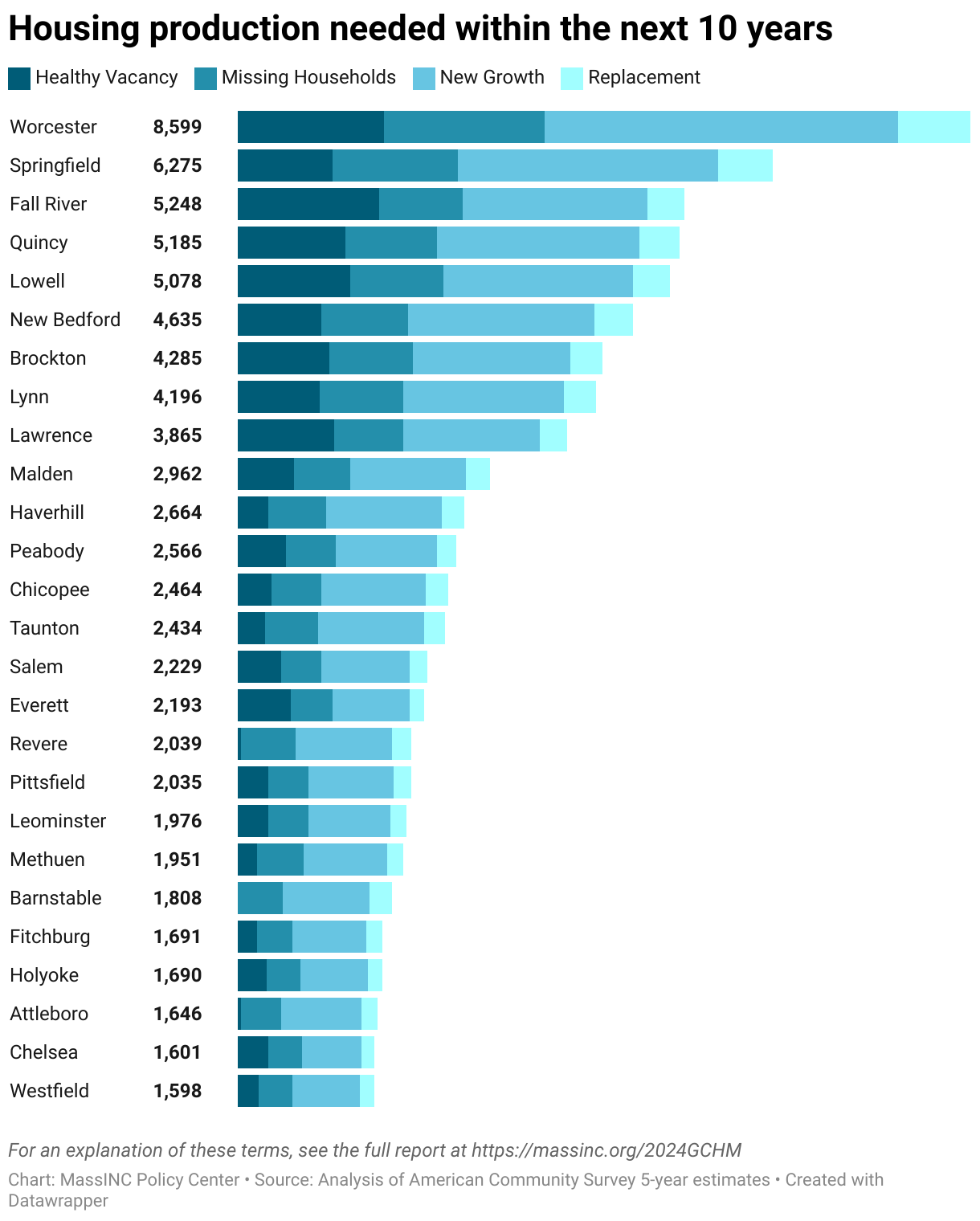

Figure ES.1 – Estimated housing production needed over next 10 years

Key Findings: Special Analysis

To address the immediate housing shortage for current residents, Gateway Cities need roughly 36,000 additional homes.

In addition to the 36,000 unit housing shortage in Gateway Cities, there is a 20,000 unit shortage in their suburbs. While there is no clear regional pattern to the shortages in Gateway Cities, estimates for their suburbs show larger shortages closer to Boston.

Anticipating future population growth and housing obsolescence, Gateway Cities should aim to produce 83,000 new homes in total over the next 10 years.

This total includes 36,000 units to meet the current shortage; 39,000 units to accommodate projected (5 percent) household growth over the next 10 years; and 8,000 units to replace those lost to obsolescence.

Currently, the largest shortages in Gateway Cities appear to be of apartments for the lowest-income households as well as rental and homeownership opportunities for middle- and upper-income households.

The 26 Gateway Cities have 35,000 more extremely low-income renters than they have apartments that are affordable to this population. These communities are also home to 50,000 middle- and upper- income renters who can afford to pay significantly more for housing and might choose to do so if attractive apartments were available in the market at higher price points. Of these 50,000 middle- and upper-income households, 16,600 would need to become homeowners for those income groups to reach the state average homeownership rates by percent of area media income.

Section 1 – Housing Production

This section shows how household growth outpaced housing stock growth over the past decade, tightening markets and reducing vacancy rates across the Gateway Cities.

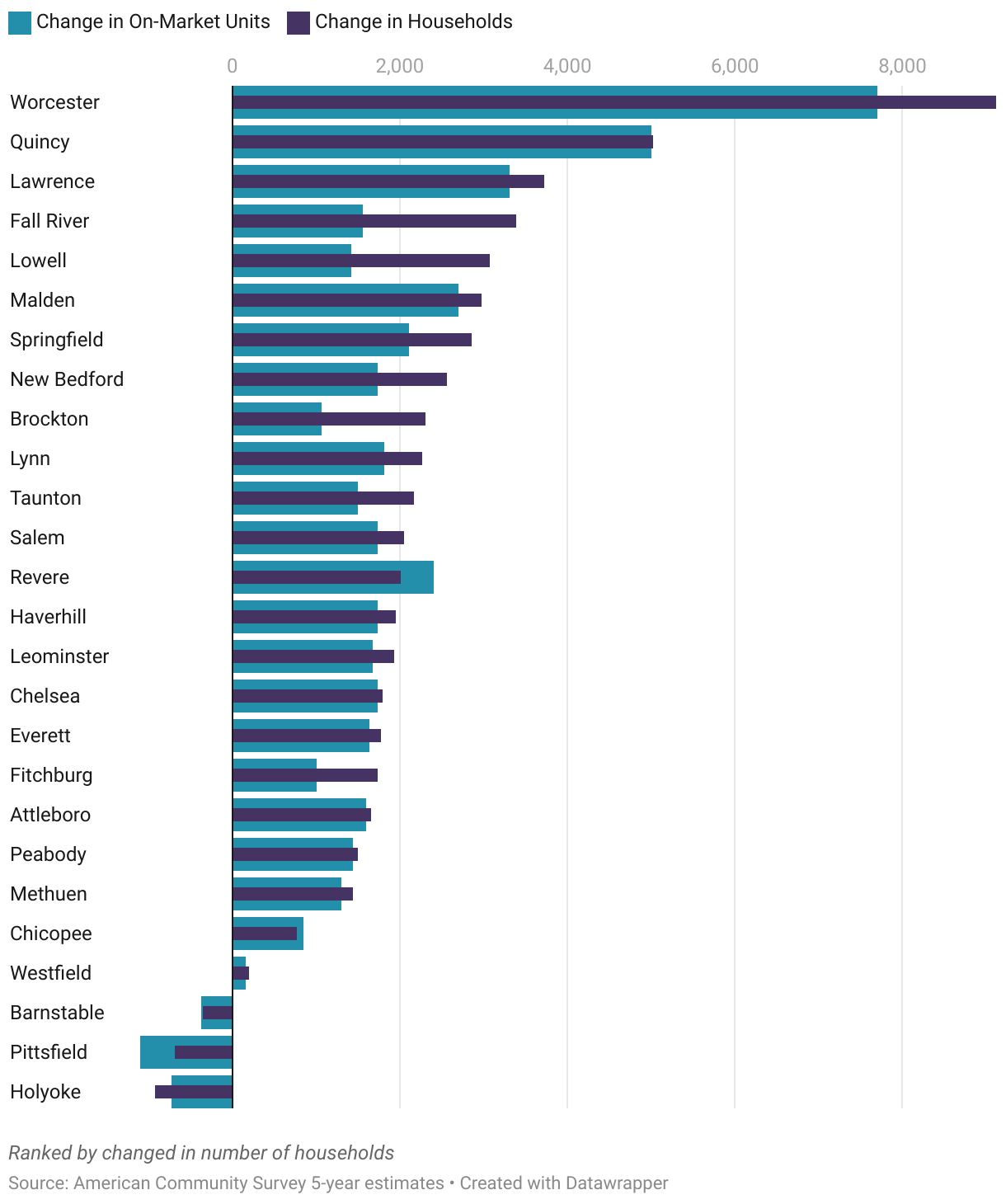

Figure ES.2 – Household growth and net on-market housing unit growth, 2012–2022

Key Findings: Housing Production

Between 2012 and 2022, Gateway Cities created over 40,000 new homes and their suburbs added more than 42,000 new homes.

Nearly all of the Gateway Cities (23 of 26) grew their housing stock over the past 10 years. While multifamily buildings did account for a large majority of housing unit growth, data from assessors show that detached single-family homes represented the majority of new buildings (63 percent). About 10 percent of the growth in Gateway Cities came from long-term vacant properties that were brought back into the market.

Household growth outpaced housing stock growth by nearly 16,000 households in Gateway Cities and over 6,000 households in their suburbs.

Between 2012 and 2022, the housing stock in both Gateway Cities and their suburbs grew by 5 percent. But the number of households increased at an even faster pace—8.2 percent in Gateway Cities and 6.7 percent in the suburbs.

With household growth exceeding growth in supply, residential vacancy rates fell in Gateway Cities and their suburbs.

In Gateway Cities, vacancy rates fell sharply between 2012 and 2015 as communities recovered from the foreclosure crisis. In Gateway City suburbs, vacancy has steadily declined since 2012, with a particularly steep drop in 2020.

Gateway Cities have enough vacant units that are not on the market to address nearly two-thirds of the estimated housing shortage.

Across the 26 Gateway Cities, there are over 23,000 vacant units in the “other vacant” category. These are generally long-term vacant units that often need considerable rehabilitation to be fit for occupancy. Reclaiming these vacant properties would go a long way toward addressing the immediate 36,000-unit housing shortage.

Section 2. Housing Affordability

This section explores housing affordability for residents of Gateway Cities in both the rental and for-sale markets. Despite significant variation in rent across these cities, the analysis finds that a large proportion of renters face heavy cost burdens and that for-sale housing is out of reach for most residents in nearly all of these communities. This section also describes the state of the affordable housing inventory in Gateway Cities and their suburbs, including both naturally- occurring and deed-restricted units.

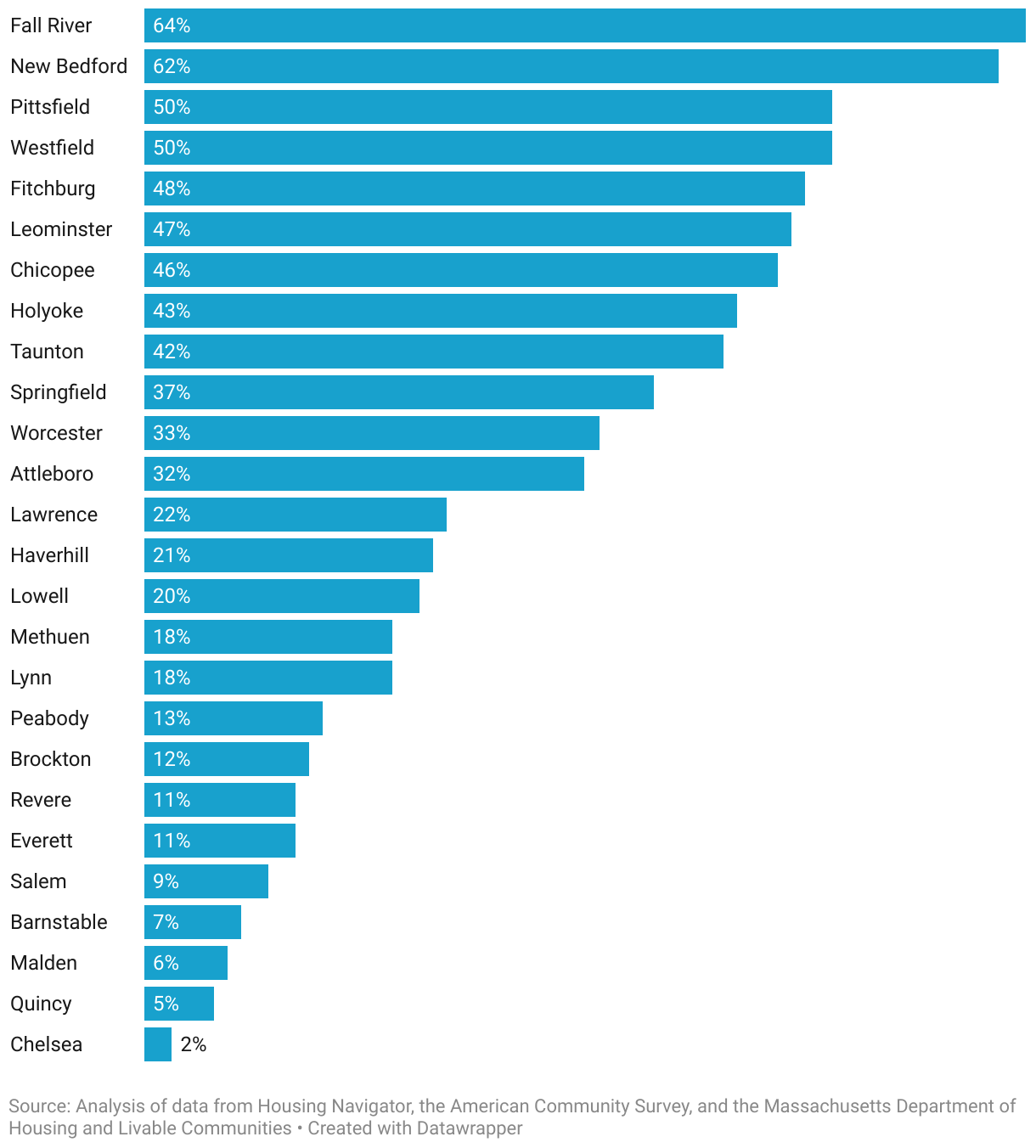

Figure ES.3 – Naturally-occurring affordable housing as a share of all rental units, 2022

Key Findings: Housing Affordability

Asking rents vary considerably across the state’s Gateway Cities, with apartments in the most expensive cities costing twice as much as those in the least expensive cities.

In July 2024, typical asking rents ranged from $1,350 in Holyoke to $2,878 in Malden.

Across Gateway Cities, half of renters are cost-burdened, and there is little discernable geographic pattern.

On average, half of Gateway City renters spend more than 30 percent of their income on rent and one-quarter spend more than 50 percent. Proximity to Boston has little influence on the share of renters experiencing housing cost burdens. On average, the median renter in Gateway Cities would need to earn $38,000 more to afford current asking rents.

Gateway Cities are home to nearly two- thirds of the state’s naturally-occurring affordable housing stock, but this inventory is dwindling.

Many of the older market-rate homes in Gateway Cities rent at amounts that are relatively affordable. Defining “naturally-occurring affordable housing” as unsubsidized units affordable to households making under 50% of state median income, our estimates show this type of housing represents 46 percent of all the affordable housing (subsidized and unsubsidized) in Massachusetts. In Gateway Cities near Boston, this reservoir of affordable housing has mostly been depleted, but naturally-occurring affordable housing still makes up half or more of the apartments in Fall River, Pittsfield, New Bedford, and Westfield.

Gateway City home values are rising faster than rents. Current prices put homeownership out of reach for three out of every four Gateway City residents.

Over the past year, the average Gateway City home price rose by 5.5 percent. In contrast to rent burdens, the affordability of for-sale housing varies considerably across cities, with large regional variation. In Malden, just 5 percent of residents can afford the average-priced home, whereas in Holyoke homes are affordable to more than half of residents. While deed-restricted affordability provisions protect roughly one in every five apartments in Gateway Cities, deed-restricted homeownership units make up less than half a percent of the owner-occupied and for-sale housing in these communities.

Section 3. Conditions for Growth

This section models pro formas for residential development to show how the high cost of construction currently makes it economically challenging to produce new housing in Gateway Cities across the state. While an analysis of regulatory and residential development policies in these communities shows that Gateway Cities have instituted a variety of policies to lower the barriers to construction, most could go further still.

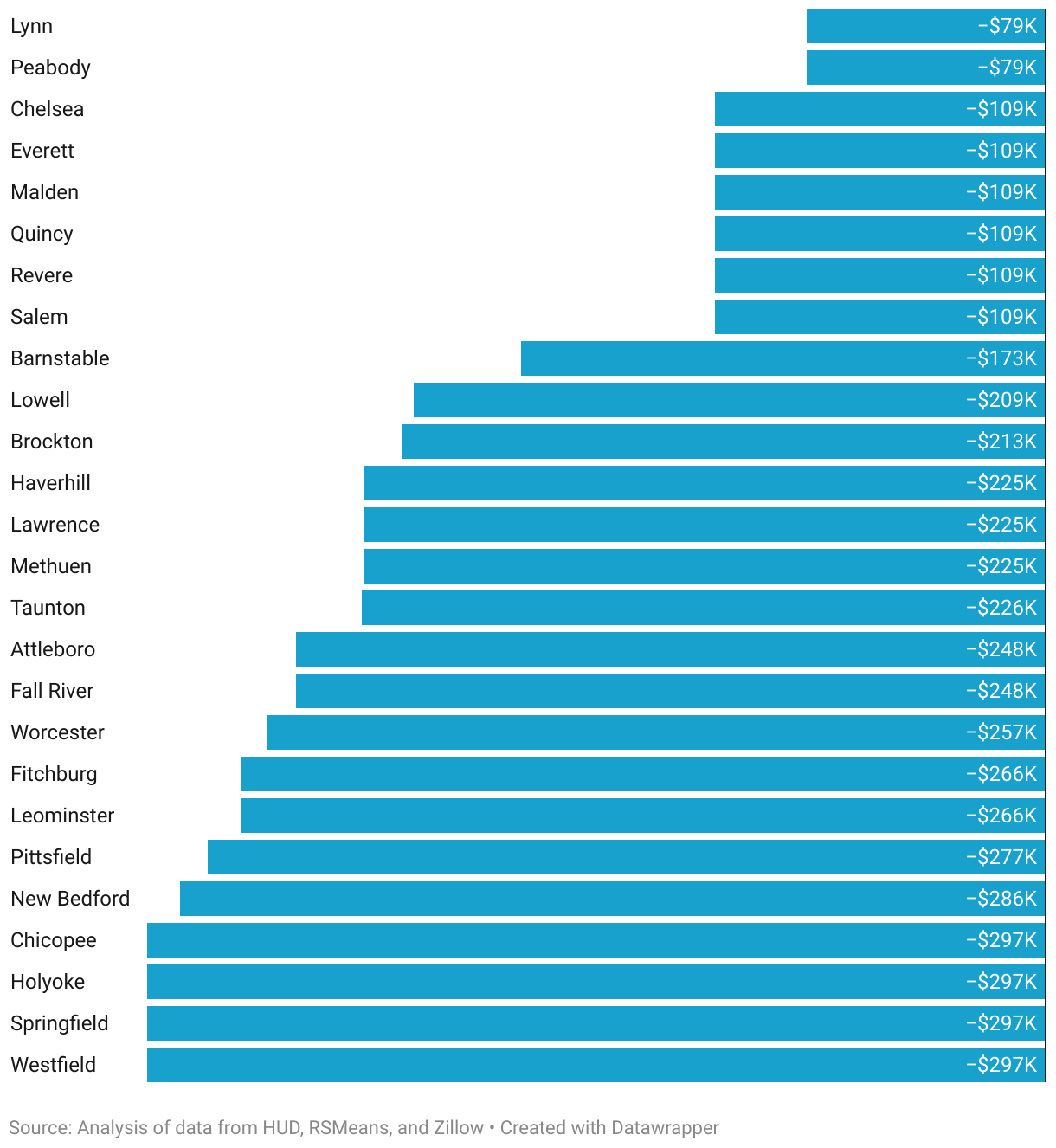

Figure ES.4 – Estimated financial gap to construct rental units, 2024

Key Findings: Conditions for Growth

A sizeable financial gap makes it difficult to build new rental units in Gateway Cities without public subsidy.

While this gap exists in all Gateway Cities, it is three times larger in the cities furthest from Boston. In the Western Massachusetts Cities— including Chicopee, Holyoke, and Springfield— each new apartment costs almost $300,000 more to produce and operate than capitalized rental income will cover. Gateway Cities near Boston have much smaller financial gaps, but apartments in Lynn, Peabody, and Malden still cost about $80,000 more to produce and operate than rents can offset.

While there is also a significant financial gap for homeownership units in most Gateway Cities, it is roughly half as the gap for rental units.

For new condominiums, the estimated financial gap is less than $150,000 per unit in nearly all Gateway Cities. Our analysis suggests that in nine cities, condominiums can be built and sold at a profit without gap-filling subsidy.

Some locally-imposed regulatory barriers likely contribute to the financial gap. However, Gateway Cities are making considerable effort—including by using municipal funds for affordable housing—to close the financial gaps on projects.

On the regulatory barrier side of things, most notable is that only three Gateway Cities currently allow for the construction of triple-deckers by- right in their residential neighborhoods. But on the pro-housing growth side, there are many bright spots. Most Gateway Cities have abated municipal taxes to spur housing development. More than half have established local affordable housing trust funds. And half provide density bonuses or other forms of regulatory relief to affordable housing projects.

Gateway Cities have significant potential for transit-oriented development.

Over the past 10 years, an average of 30 percent of the new housing that was built in Gateway City communities with commuter rail service was constructed within half a mile of a station. There is considerable opportunity to continue infill development in a manner that gains even more leverage from the state’s existing transit infrastructure. In most Gateway Cities, the majority of census block groups fall into the “above average walkable” or “most walkable” categories. In eight Gateway Cities, more than one-third of census block groups fall within half a mile of a commuter rail station. In 17 of the 26 Gateway Cities, every census block group is located within half a mile of an MBTA or RTA bus stop.

Section 4. Neighborhood Revitalization

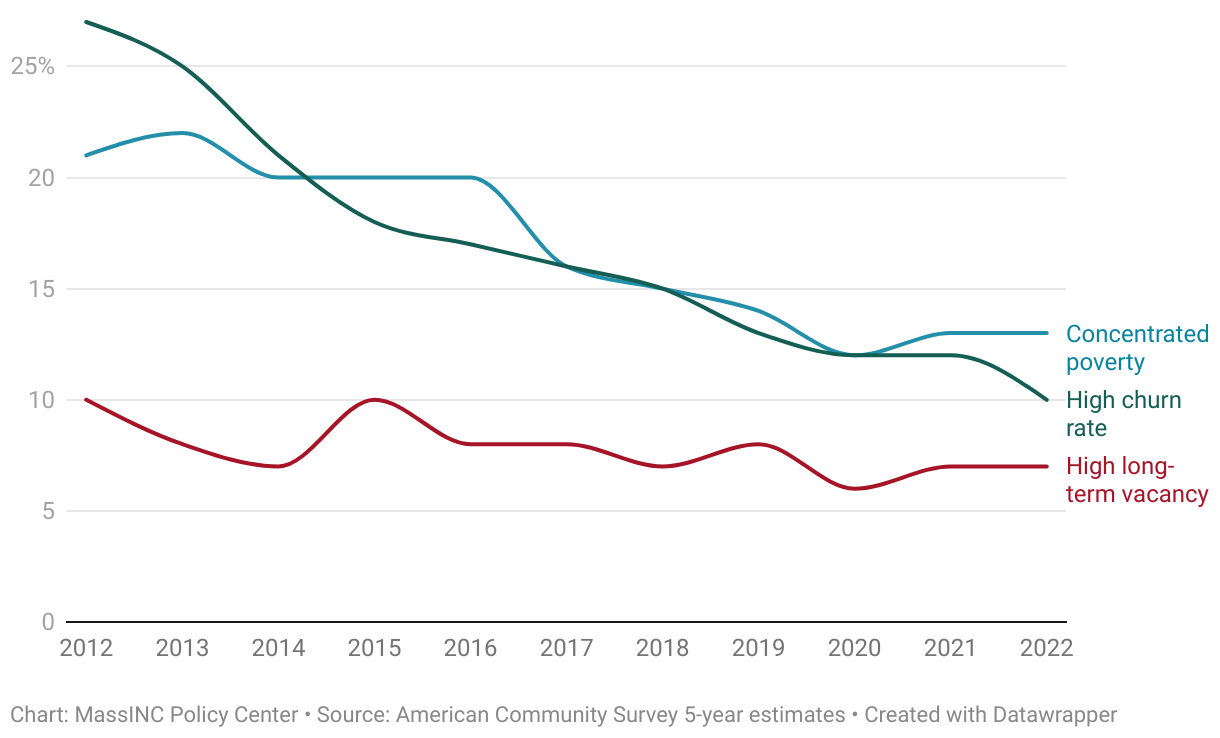

Trends presented in this section suggest most Gateway City neighborhoods are on a stable to improving course, though several continue to struggle with extreme concentrations of poverty and blighted property.

Figure ES.5 – Share of census tracts in Gateway Cities by indicator of neighborhood health, 2012–2022

Key Findings: Neighborhood Revitalization

The gap between local and state median income has remained relatively constant for most Gateway Cities over the past 10 years.

On average, median household income (MHI) in Gateway Cities inched closer to the statewide average by just one percentage point, moving from 75 percent of state MHI in 2012 to 76 percent in 2022. Cities closest to Boston did see more significant gains, but overall regional variation is relatively small.

Though it still presents a major concern for several Gateway Cities, concentrated poverty has fallen significantly since the Great Recession.

From 2012 to 2022, the share of census tracts in Gateway Cities with poverty rates over 30 percent fell from 21 percent to 13 percent. Still, nearly 200,000 Gateway City residents live in neighborhoods with poverty rates over 30 percent. In Holyoke and Springfield, about one in every three residents lives in neighborhoods with this level of concentrated poverty.

Residential stability has increased dramatically in Gateway Cities; the number of neighborhoods with high levels of vacant and blighted property is slowly trending down.

Across Gateway Cities, the share of census tracts where more than one-fifth of residents moved within the past 12 months has fallen steadily, from 27 percent in 2012 to 10 percent in 2022—a trend that started long before the COVID pandemic. The share of Gateway City census tracts where more than 8 percent of housing structures are classified as long-term vacant fell from 10 percent in 2012 to 7 percent in 2022. (Studies indicate that long-term vacancy presents a serious concern when it exceeds this 8 percent threshold.)

Section 5. Equitable Development

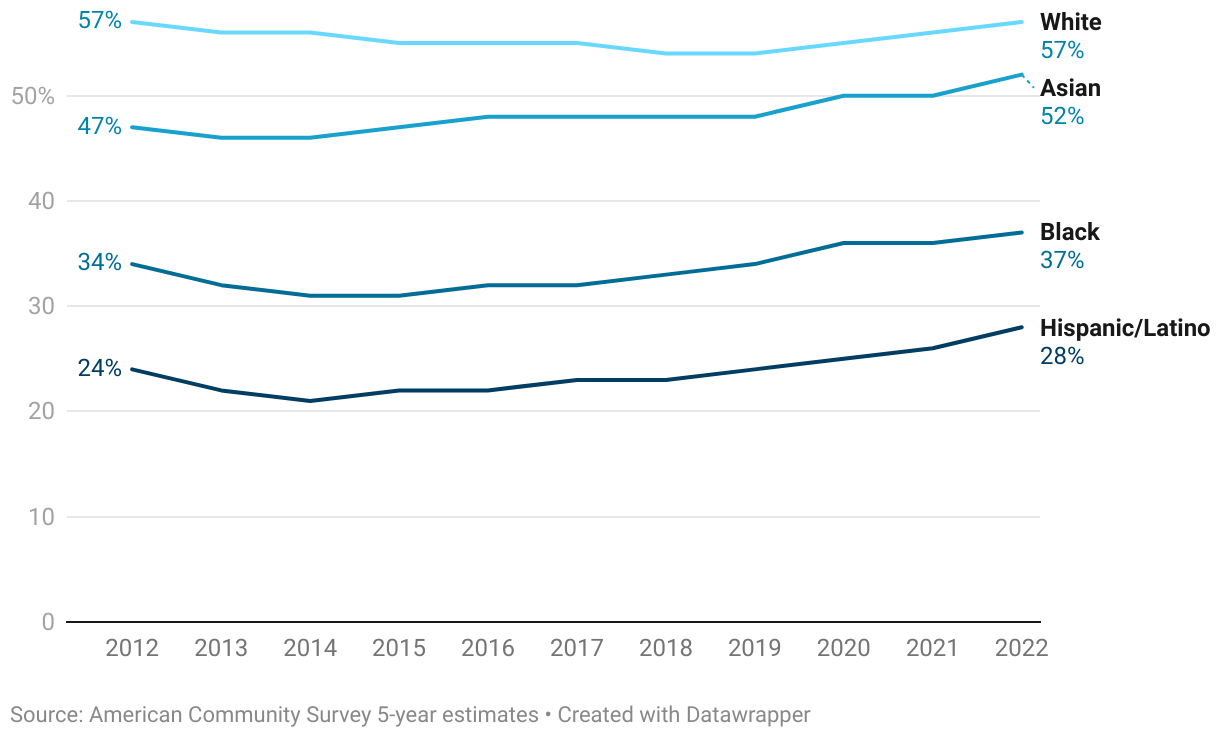

The evidence in this section suggests that the markers of gentrification are mostly absent in Gateway Cities, with the exception of those adjacent to Boston. It also uncovers positive equitable development trends with respect to homebuyers of color and property values in Gateway City neighborhoods of color.

Figure ES.6 – Homeownership rates by racial/ethnic group, Gateway City 5-year rolling average, 2012–2022

Key Findings: Equitable Development

Homeownership rates have held steady in most Gateway Cities across building types.

Over the past 10 years, the homeownership rate for Massachusetts residents who live in Gateway Cities has remained virtually unchanged at 49 percent. In 2022, nearly 90 percent of single- family homes were owner-occupied, and 70 percent of two- and three-family homes had an owner-occupant in one of their units. These are about the same rates as 2012, which dispels some concern about increased investor activity in an important segment of the Gateway City housing market.

Homeownership rates are rising for residents of color in Gateway Cities, but they remain substantially lower for residents of color than for White residents.

Between 2012 and 2022, the White homeownership rate held steady at 57 percent, while the Black homeownership rate rose 3 percentage points to 37 percent. During that period, the Asian and Hispanic homeownership rates increased by 5 percentage points each, rising to 52 percent and 28 percent, respectively.

Homes values remain lower in Gateway City neighborhoods of color, but prices are appreciating faster in those neighborhoods than in majority-White Gateway City neighborhoods.

Property values in Gateway City neighborhoods where residents of color make up more than half the population are roughly $100,000 lower, on average, than in majority-White Gateway City neighborhoods. However, home values rose by 276 percent in neighborhoods of color, slightly faster than the 234 percent increase in majority- White neighborhoods between 2012 and 2022.

In almost all Gateway Cities, new residents are no more likely than established residents to have incomes above $75,000.

Concerns about gentrification are often based on the theory that higher income renters pushed out of Boston are moving to Gateway Cities and competing with Gateway City residents for apartments. With the exception of Everett, Malden, and Revere, Gateway City newcomers have slightly lower incomes than people who have lived in these communities for longer.

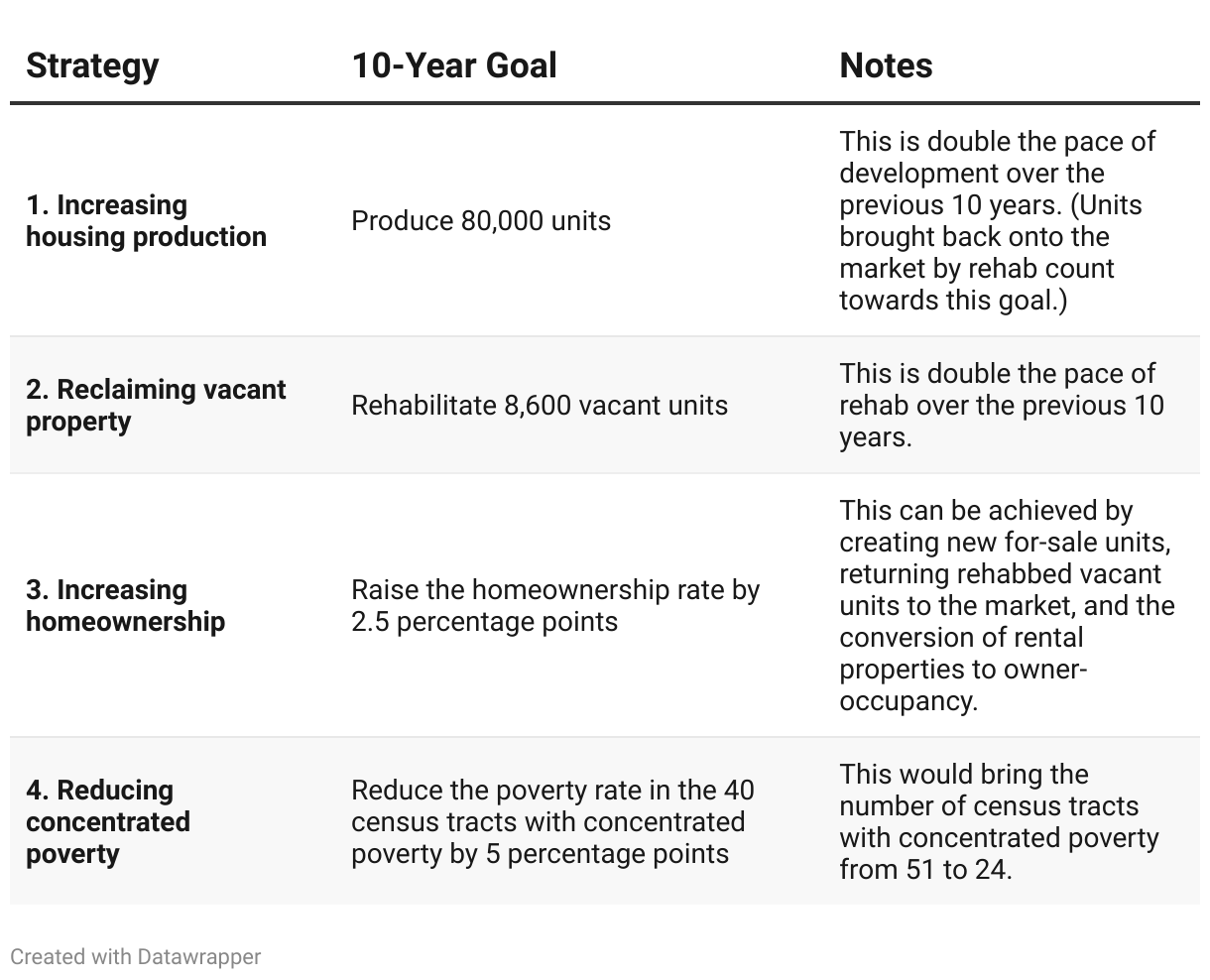

Section 6. Data-Driven Goals and Strategic Action

To produce the quantity of housing required, Gateway Cities must stimulate private investment in residential development in a manner that best serves the varied needs of their residents. Toward these ends, this final section describes high-level goals and potential strategies to achieve them in four interrelated categories: new housing production, vacant property reclamation, homeownership creation, and concentrated poverty reduction. While this summary presents strategies for Gateway Cities as a group, variation among communities translates into variation in the relative importance of each of these objectives, as noted throughout the report. State and local leaders must find solutions that target these varying strategies in proportion to the local need.

Figure ES.7 – Summary of goals by strategy

1. Increase housing production

Goal: Produce 80,000 new units in our Gateway Cities by 2035.

Potential Strategies:

- Provide more “shallow subsidies” to make market-rate residential projects economically feasible.

- Assemble, clean, and pre-permit land for multifamily residential development.

- Make it possible to build triple-deckers and duplexes by-right.

- Create predictable policies around municipal tax abatement for affordable housing.

- Develop and execute a regional construction workforce strategy.

- Support emerging developers through both local initiatives and state incentives.

- Partner with suburban neighbors to develop and execute regional housing strategies, particularly with regard to serving extremely low-income households.

2.Reclaim vacant property

Goal: Rehabilitate 8,600 blighted/vacant units by 2035.

Potential Strategies:

- Increase state investment in vacant property acquisition and rehabilitation.

- Reassess the state’s rehabilitation building code.

- Utilize the new receivership statute.

- Clarify the new municipal tax lien foreclosure statute.

3. Increase homeownership

Goal: Raise the Gateway City homeownership rate by 2.5 percentage points by 2035.

Potential Strategies:

- Develop local homeownership targets and strategies with a focus on closing racial and ethnic homeownership gaps.

- Build more affordable homeownership opportunities using the shared equity model.

- Expand and enhance programs to help households move from subsidized rental housing to affordable homeownership.

4. Reduce concentrated poverty

Goal: Reduce the poverty rate by 5 percentage points in the 51 Gateway City census tracts with concentrated poverty by 2035.

Potential Strategies:

- Redevelop public housing into mixed-income communities.

- Develop a regional strategy and complementary state policy to produce more housing for extremely low-income households in areas with lower poverty rates.

Concluding Thoughts: Building the Capacity to Mount an Effective Response

There is no single step that Gateway Cities can take to help Massachusetts build its way out of this housing shortage, while also working to ensure that new growth meets the multiple housing needs of their neighborhoods and residents. Our survey of Gateway City housing policies shows that communities are already employing a variety of best practices to stimulate development and reclaim vacant property. However, no city has been able to implement numerous strategies all at once. This is largely a matter of capacity. Gateway Cities have limited staff and resources. While CDCs can complement and magnify municipal capacity, many Gateway Cities lack these key partners. Mounting an effective response to the housing crisis will require considerable attention to capacity building in local government, state agencies, and nonprofits. As policymakers consider how the action items outlined above could play a role in the state’s housing strategy, they must prioritize capacity building to ensure Gateway Cities are equipped to utilize these tools and execute the plan effectively.