Findings from the Special Analysis section of the 2024 Gateway City Housing Monitor show that the balance between rental and ownership housing affects the scale of the housing shortage, the amount of public subsidy required to close financial gaps, and the level of unmet demand for homeownership. This year’s Special Analysis digs deeper into homeownership—particularly the availability and production of for-sale units. A “supply-side” view helps us understand how the geography of homeownership relates to key equitable development principles, such as economic mobility, social inclusivity, community wealth building, and protection from displacement.

This section begins with data and evidence to make the case for strategic efforts to increase the supply of for-sale housing. Part 2 sizes up the need by mapping “homeownership deserts” with especially low homeownership rates. Part 3 examines the barriers to developing more for-sale units in these communities, including the lack of state resources to help overcome the hurdles. The analysis concludes with recommendations to strengthen Gateway Cities increasing the supply of homes for purchase.

1. Why Focus on Homeownership in Gateway Cities

The 2024 Gateway City Housing Monitor set a production target of 83,000 new housing units, assuming the tenure mix—the balance between rental and for-sale homes—remains constant. That assumption may be neither the most accurate nor the most desirable. Developers, guided by market forces, ultimately make tenure choices, but in Gateway Cities the heavy reliance on public subsidy to close financial gaps means state and local preferences matter. Deciding what tenure mix to pursue is not a purely technical exercise; it requires judgments about the benefits of homeownership, who should have access to it, where, and under what conditions. Those judgments inevitably rest on a broader vision of what kind of communities we want to build.

What We Learned From the 2024 Housing Monitor

The following findings from the 2024 Gateway City Housing Monitor highlight how adjustments to the tenure mix can address the housing shortage, reduce costs, and unlock pent-up demand for homeownership:

- Simply producing an ownership unit in place of a new rental unit reduces the overall housing shortage. Because the vacancy rate needed to stabilize prices in the for-sale market is lower compared to the rental market, fewer net new housing units are needed if ownership grows as a share of the housing stock. If Gateway Cities with owner-occupancy rates below the statewide average of 65 percent focused their efforts on incentivizing the supply of ownership units, as many as 35,000 of the 83,000 units that need to be created by 2032 could be additional ownership units. Compared to the scenario in which the tenure mix of households remains constant, 1,000 fewer housing units would need to be produced. 1

- For-sale units have a smaller financial gap, reducing the amount of public subsidy needed to meet our housing production needs. Our analysis shows that the financial gap for condominiums is smaller than for rentals (see Chapter 3: Conditions for Growth). In 2024, we estimated that in a high ownership production scenario, the smaller financial gap combines with a lower production target to reduce the aggregate financial gap to meet Gateway City housing supply needs by as much as $2 billion (40 percent).2

- Unmet demand for homeownership artificially inflates the demand for rental units, limiting options and making apartments more expensive for those who need them most. In 2022, Gateway Cities had 50,000 middle- and upper-income households (those earning 80 percent or more of area median income, or AMI) that are paying significantly less for rent than they can afford. Low rent is likely a selling point to live in these communities, but some of these households may prefer to own, if there were more attractive options. By comparing homeownership rates by income group to those same rates for the state as a whole, we estimated that there is an unmet

,internal “latent demand” for about 600 housing units affordable to households making between 80 and 100 percent of AMI and 16,000 housing units affordable to households making over 100 percent of AMI.3

Research-Backed Benefits of Homeownership

Beyond the immediate implications for housing production to stabilize prices, there are deeper reasons to support a better balance between rental and ownership. A growing body of academic research points to the social, economic, and civic benefits of homeownership.

- The geography of homeownership plays a critical yet often overlooked role in contributing to income

–segregation, shaping economic mobility and pathways to the middle class. Raj Chetty and colleagues show that the neighborhood where a child grows up has a powerful influence on future earnings, with children from high-poverty areas earning less as adults than peers raised in communities with lower poverty rates.4 These neighborhood effects are reinforced by housing tenure structures: The balance of ownership and rental housing both reflects and reproduces patterns of segregation. Stratification in housing by type—through zoning, housing stock, and ownership patterns—predicts and entrenches income segregation, sorting families by income across neighborhoods.5This stratification is at least partially a choice; regulatory barriers and discriminatory practices by private actors shape the development of housing, embedding inequality in the housing market itself.6The result is a fractured geography of housing opportunity, where access to homeownership does not just mirror inequality but amplifies it. - Homeownership functions as self-imposed rent control. For many households, homeownership is a form of cost stabilization. Mortgage payments—especially for fixed-rate loans—are predictable, while renters face ongoing risks of rent increases, no-fault evictions, or unaddressed housing quality issues that precipitate a move. This autonomy and predictability contribute to reduced stress, greater satisfaction, and long-term health benefits.7

- Homeownership supports school stability and performance. When families move frequently—as is more common in neighborhoods dominated by rental housing—schools face higher student turnover, which disrupts learning continuity, challenges classroom management, and complicates planning for resources and staffing. Prior research has found that higher student mobility within schools is associated with lower academic achievement for both mobile students and their classmates.8

- There are civic benefits to homeownership. Homeownership is also linked to higher levels of civic engagement, including voting, volunteering, and participating in local organizations.9 While some of this may be due to selection effects, homeownership provides a form of rootedness that often translates into greater personal investment in local governance and community well-being.

- Homeownership allows families to directly benefit from community revitalization. Investments in neighborhood infrastructure, schools, or revitalization are capitalized into property values. Renters often face higher rents when this occurs, but homeowners gain equity, creating a direct financial stake in local progress. This mechanism—highlighted in community wealth– building frameworks and supported by urban economics research—underscores how homeownership not only provides stability but also enables households to share in the value generated by collective neighborhood improvements.10

Why a Balance is Needed

Of course, there are also downsides to too much homeownership. “Rental deserts”—neighborhoods dominated by owner-occupied housing—can contribute to income and racial segregation, limit labor market mobility, and exclude people who need housing that offers affordability or adaptability rather than long-term commitment. A balance of rental and ownership options allows people to put down roots and invest in their communities, while also making room for newcomers and long-time residents who require flexibility at different life stages.

Much of the recent policy in Massachusetts has focused rightly on expanding rental options in areas where exclusionary zoning and local resistance have created barriers to new multifamily development. But we must not lose sight of the other side of the same coin. In Massachusetts, many Gateway Cities are better described as “ownership deserts”—places where renting is common, but opportunities for homeownership are scarce. Addressing this imbalance fills a critical gap in our understanding of the state’s housing dynamics and offers an opportunity to design more equitable and economically vibrant communities.

Spotlight: OneHolyoke CDC harnesses the power of duplexes to expand homeownership

OneHolyoke has delivered more than 160 affordable homeownership units in the city, the majority built as duplexes with one ownership and one rental unit. From a financial standpoint, the model works on two levels: Rental income provides financial stability for families living close to the margin, and it allows the organization to “reverse engineer” sale prices based on both household income and expected rent. This flexibility has made duplexes a cornerstone of OneHolyoke’s strategy, keeping homeownership affordable while also providing the benefits of owner-occupied rental housing. Most projects have been financed with federal HOME funds, which require buyers to earn less than 80 percent of AMI at the time of purchase and to live in the property as their primary residence. Landlords must certify that their tenants also meet income limits, and OneHolyoke maintains light-touch oversight by being listed on the insurance policy and checking in annually.

Tenure Mix as a Tool to Reduce Concentrated Poverty

US housing policy has long grappled with how to reduce the harms of concentrated poverty. Much of the emphasis has been on mobility strategies—rental vouchers or programs like Moving to Opportunity—built on the premise that families advance by leaving distressed neighborhoods for so-called “high-opportunity” areas. Yet this approach leaves behind the many families who remain. In places like Massachusetts’s Gateway Cities, where a large share of low-income households is concentrated, the central challenge is ensuring that all neighborhoods become high-opportunity places in their own right. Federal initiatives such as HOPE VI and Choice Neighborhoods have attempted to meet this challenge by redeveloping distressed public housing into mixed-income communities, and states and cities have added their own tools. However, in most cases, these overwhelmingly produced mixed-income rental housing rather than a balanced tenure mix more reflective of overall housing supply.11

In contrast, the UK and parts of Europe have targeted tenure mix—the balance between rental and ownership units—to encourage economic integration. The evidence on these initiatives is uneven; by and large studies on tenure mixing are of varying quality, produce contradictory results, and are often overly general, failing to account for differences in approach or context.12A substantial portion of the available literature is based on the UK’s largest tenure diversification effort: Margaret Thatcher’s Right to Buy scheme. It is important to note that each new unit of homeownership under Right to Buy came at the direct expense of an existing publicly-owned affordable rental, and thus did not contribute to broadly shared quality of life improvements.

However, it does seem clear from the evidence that simply adding homeowners does not automatically yield stronger communities. Interaction across income groups often remains limited unless intentionally fostered through design, services, or programming. In hot housing markets, the threat of gentrification and displacement is a real concern. Yet positive impacts have been documented, including improvements in public safety, better neighborhood conditions and self-image, and in some cases, greater civic engagement and investment.

Research from the Brookings Institution points to how tenure diversification can be done right. Looking at thousands of neighborhoods over 15 years, researchers identified nearly 200 places across the country where concentrated poverty declined dramatically without community displacement.13These “inclusive prosperity” neighborhoods shared a cluster of characteristics, and one of the most predictive was a higher rate of homeownership. Other important indicators included increasing housing density, lower levels of residential vacancy, higher rates of self-employment, and the presence of community-building organizations.

It is worth zooming in on the interrelationship between the role of homeownership and an expanding housing supply in the Brookings findings. Displacement, at its core, is a math problem: If higher-income households move in without new housing being added, lower-income renters get pushed out. The UK’s Right to Buy is a cautionary example—diversifying tenure by converting rentals into ownership shrank the affordable stock and left fewer options for those who relied on it. A more sustainable approach is to diversify incomes while also expanding supply, so new households can enter without displacing existing renters. In that context, expanding homeownership can work alongside affordability protections as part of a balanced strategy to stabilize households while creating stronger, more resilient neighborhoods.

Taken together, the research suggests that tenure mixing is not a cure-all. It is most effective when paired with long-term affordability, anti-displacement protections, and social investment, and when pursued as a means to expand the housing stock. While still relatively underexplored in the US, tenure mixing remains a promising tool—one that could complement mobility and rental-focused strategies by helping families build stability and opportunity in place.

Spotlight: Mixed-Tenure Housing Development in South Holyoke

Housing authorities in the United States are almost exclusively rental developers, but the Holyoke Housing Authority (HHA) took a different path in South Holyoke by incorporating affordable homeownership into a mixed-tenure project. This decision was especially significant in a neighborhood where more than 90 percent of homes were rentals, and where residents had long advocated for opportunities to own. Instead of the resistance that often greets new housing proposals, the project attracted strong community support, with neighbors welcoming the conversion of long-vacant lots into homes that would build stability and equity for local families. To make the numbers work, HHA turned to modular construction, which helped lower costs and accelerate the construction timeline, while still delivering duplex-style homes that struck the right balance between density and the community’s desire for a single-family-like neighborhood fabric. The result is a rare example of a housing authority-led development that expanded homeownership in a way that was both financially feasible and embraced by the community.

2. What It Means to Be a Homeownership Desert

To understand the importance of homeownership in Gateway Cities, we begin by defining what it means for a neighborhood to lack ownership opportunities altogether. The notion of a “desert” comes from research on food access, where the absence of grocery stores signals deep patterns of exclusion and disadvantage. Housing scholars have since applied this idea to tenure, showing how “rental deserts” limit the choices available to renter households and reinforce patterns of segregation. Flipping this lens, we focus on “homeownership deserts”—neighborhoods where less than 20 percent of the housing stock is owner-occupied.

These places matter for the same reasons that rental deserts do: They contribute to socioeconomic segregation by concentrating lower-income households in overwhelmingly rental neighborhoods. In addition, the absence of ownership opportunities undermines neighborhood stability and cuts off pathways to community wealth building. Beginning with this definition grounds our analysis in a clear standard for identifying the communities where expanding homeownership could do the most to stabilize neighborhoods and open pathways to the middle class.

See Appendix: Defining a Homeownership Desert for more information.

About the Homeownership Deserts

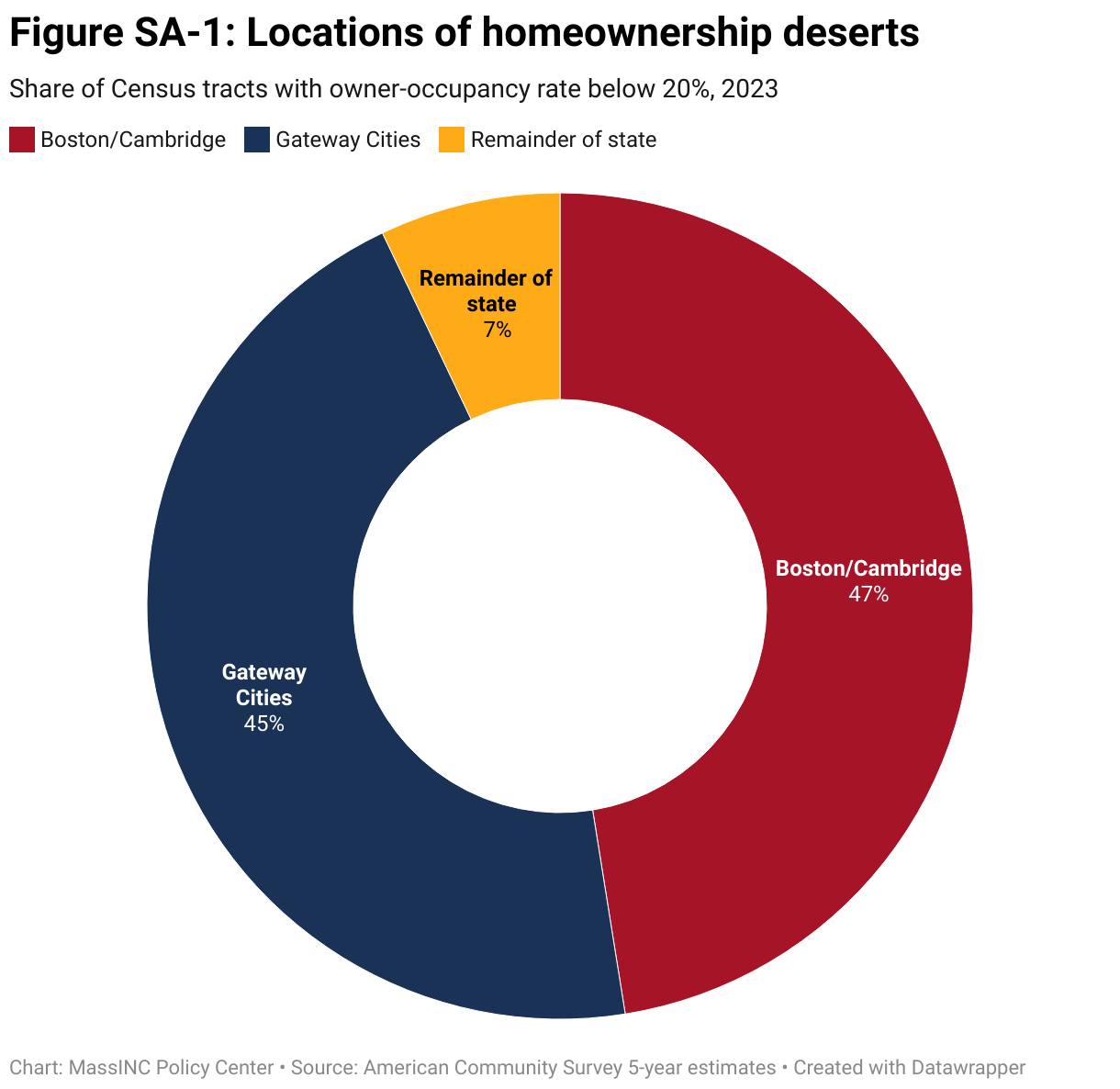

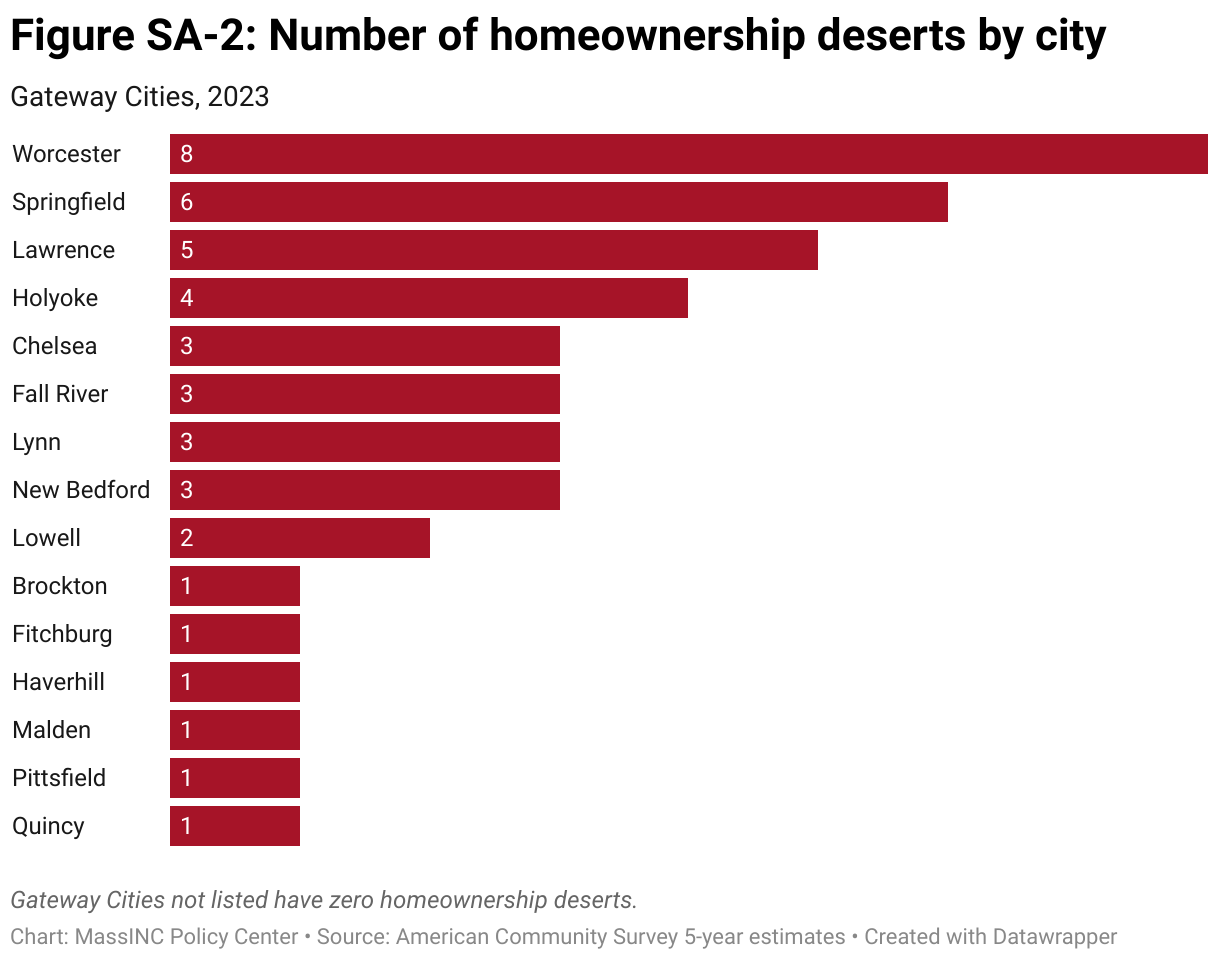

We identified 95 census tracts in Massachusetts that qualify as homeownership deserts. These areas account for 6 percent of all census tracts with at least 200 housing units. Unsurprisingly, the majority of homeownership deserts are found in cities, where rental options are more abundant. They are about evenly split between Boston/Cambridge and the Gateway Cities, with just 7 percent in the remainder of the state (Figure SA-1). Fifteen out of 26 Gateway Cities—a little more than half—have at least one homeownership desert. Worcester and Springfield have the most neighborhoods that qualify as homeownership deserts—eight and six respectively—but they are also the two largest Gateway Cities by population (Figure SA-2). Outside of the Gateway Cities and the Boston/Cambridge area, there are just seven census tracts that qualify as homeownership deserts. They are located in Bourne, Framingham, Nantucket, Somerville, Waltham, and Woburn.

The Geography of Homeownership and Poverty

In Massachusetts, the relationship between homeownership rates and neighborhood poverty is striking. On average, the poverty rate in homeownership deserts is 30 percent, while it is 9 percent elsewhere. A quantile regression analysis further confirms this: At the median, poverty rates decline from roughly 22 percent in neighborhoods with 20 percent owner-occupancy to about 6 percent in places where 70 percent of homes are owner-occupied—a 14-percentage point difference.

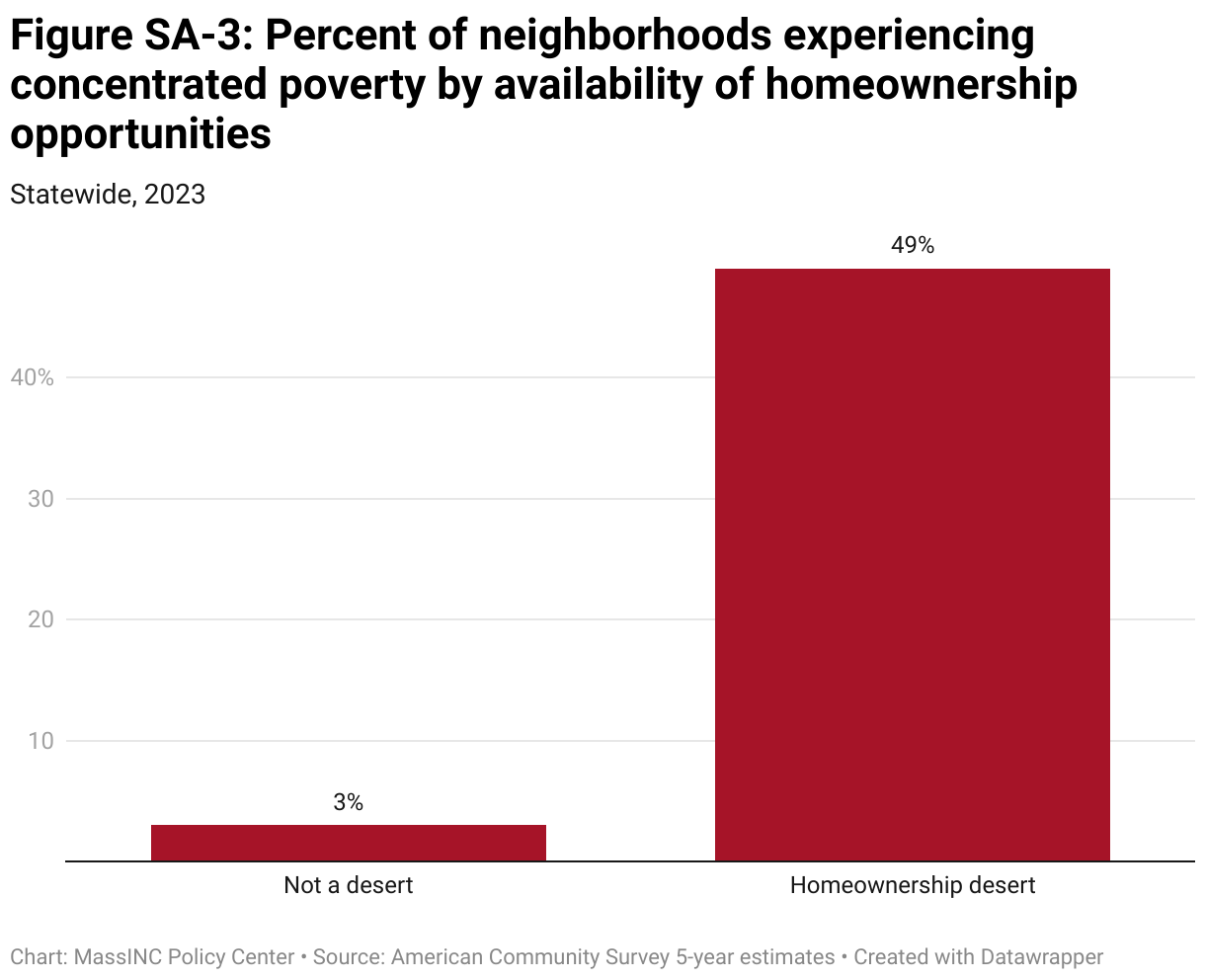

With intensifying economic segregation over the last several decades, high concentrations of poverty in urban neighborhoods have become an increasing concern. These concentrations of disadvantage reduce academic achievement, upward mobility, health, and well-being. Researchers believe lasting harm occurs when residents live in neighborhoods with poverty rates over 30 percent, which we define here as areas of highly concentrated poverty.

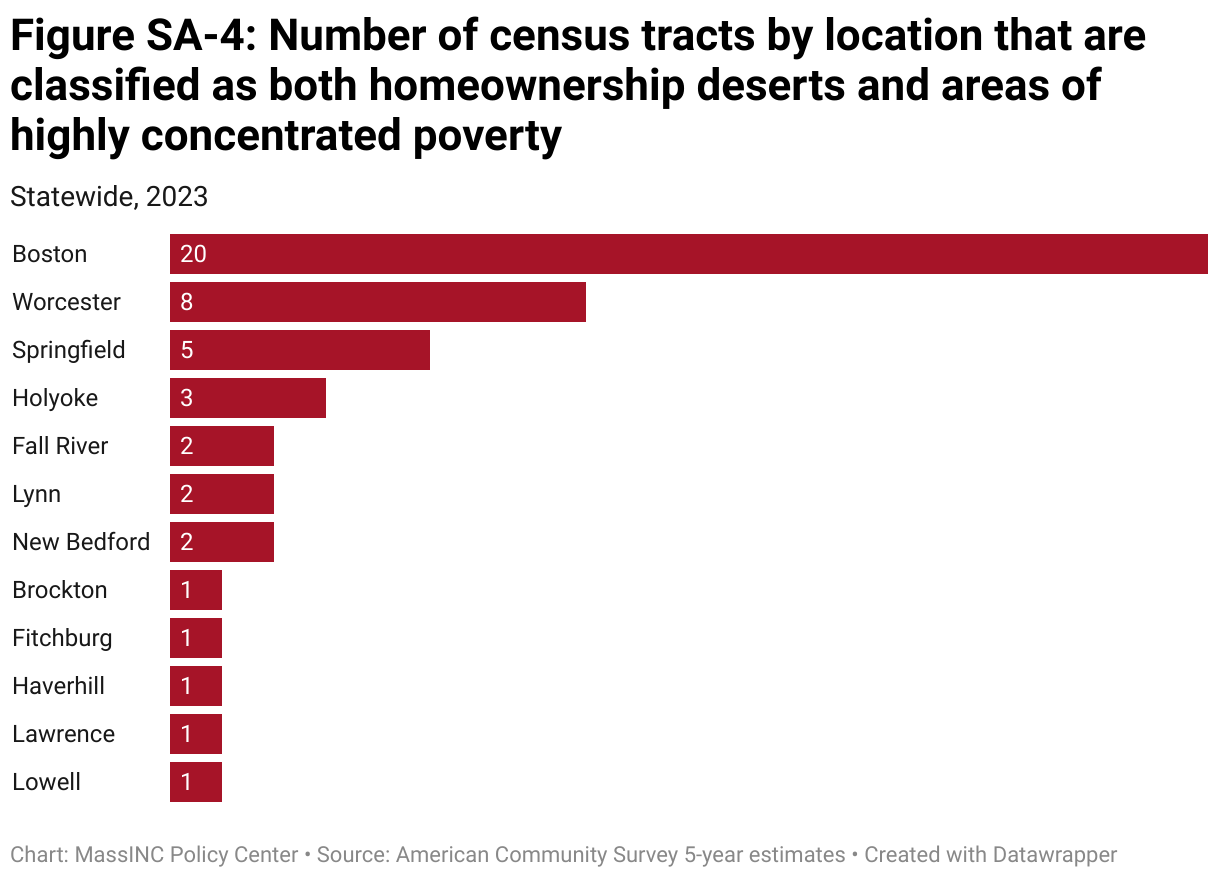

In 2023, half of homeownership deserts were also areas of highly concentrated poverty, compared to just 3 percent of other neighborhoods (Figure SA-3). This makes residents of homeownership deserts sixteen times more likely to face the effects of highly concentrated poverty. In total, there are 141,150 residents of Massachusetts living in neighborhoods that are both homeownership deserts and places of highly concentrated poverty. This combination is especially prevalent in Boston, Worcester, and Springfield—the state’s largest cities—and there are more of these neighborhoods in Holyoke, Fall River, Lynn, New Bedford, Brockton, Fitchburg, Haverhill, Lawrence, and Lowell (Figure SA-4).

Gateway Cities With a Plan to Add More Homeownership

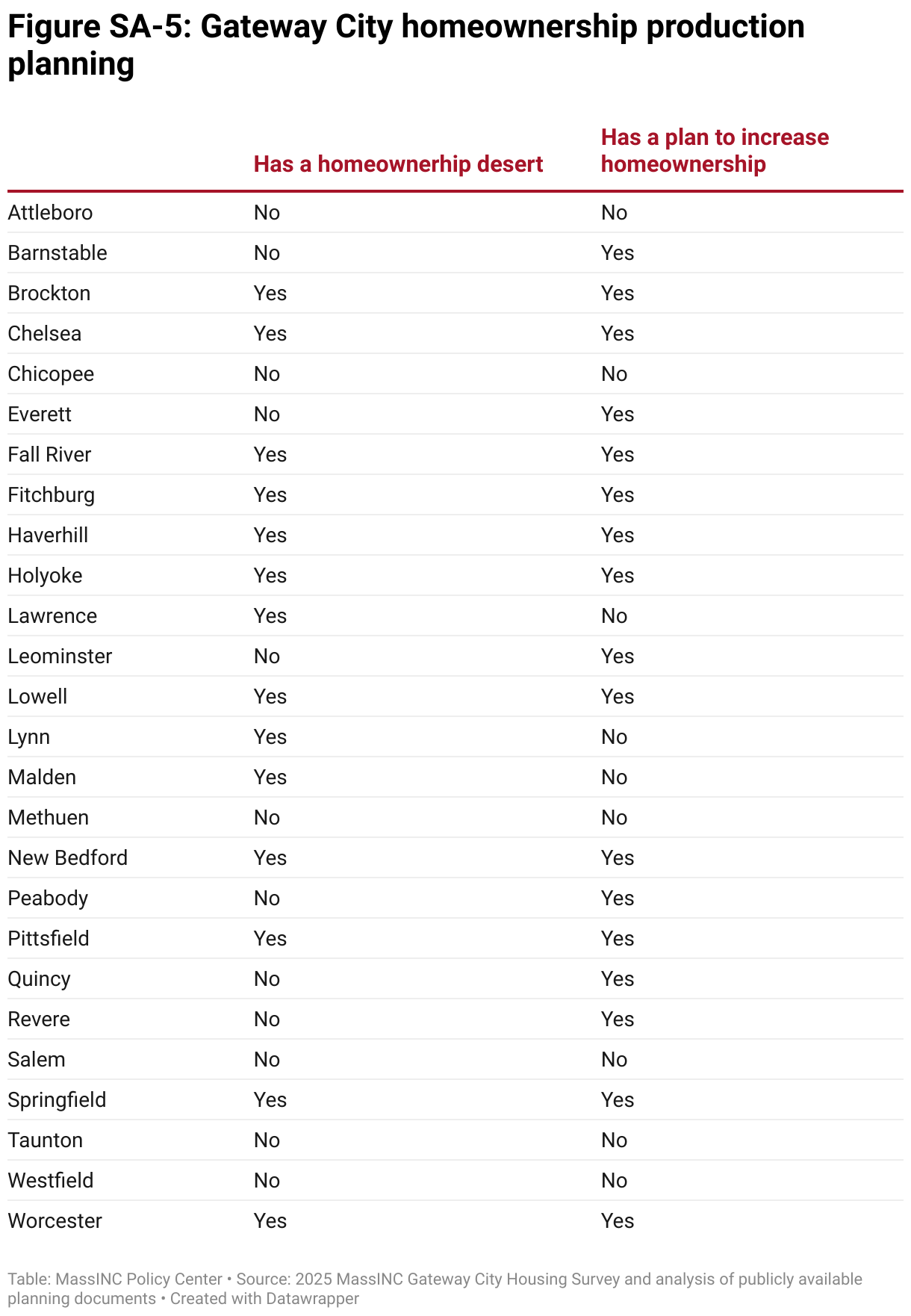

We surveyed Gateway Cities on whether they have a strategic plan to increase homeownership through the production, rehabilitation, or conversion of housing units (Figure SA-5). Nine out of 26 Gateway Cities (35 percent) responded yes to this question. Through an examination of public documents, we discovered an additional seven Gateway Cities that have housing plans that declare the need or desire to produce additional homeownership units. Taken together, at least 17 out of 26 Gateway Cities (65 percent) have indicated an intention to produce additional for-sale units, either via our survey or in public documents. Of the 14 Gateway Cities with at least one homeownership desert, all but three (Lawrence, Lynn, and Malden) have shared their intention to increase homeownership.

Examples of such statements include:

- Brockton will “(p)romote home ownership throughout the city. Actions include requiring home ownership units as part of redevelopment where practical, and supporting homeownership assistance financing programs.”14

Leominster and Fitchburg will use Community Development Block Grants and HOME funds for “(a)ffordable rental and ownership housing acquisition, development, and rehabilitation.” Furthermore, they will work with Department of Housing and Community Development to “develop ownership deed restrictions that survive foreclosure, satisfy HOME regulations, and enable units to be counted on the Subsidized Housing Inventory (SHI).”15

Lowell will “(e)xpand and create new opportunities for affordable homeownership.”16

Springfield will “(c)reate affordable homeownership opportunities through new construction and provide down payment assistance or buyer subsidy to increase affordability.”17

Worcester will “(c)reate an economically feasible pathway for the creation of affordable ownership units in the City’s inclusionary zoning ordinance.”18

3. Eliminating Homeownership Deserts

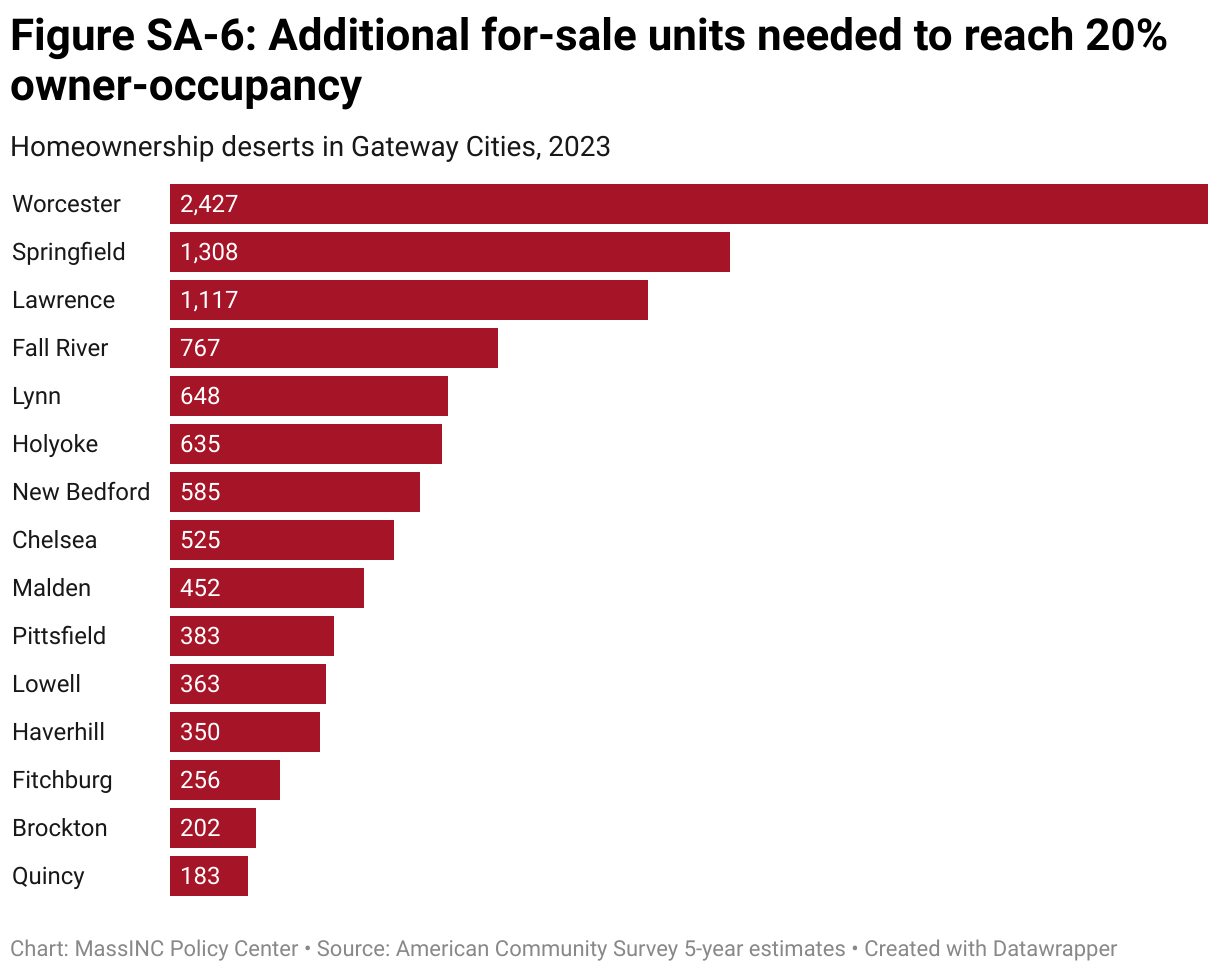

We calculated how many additional homeownership units each Gateway City would need to push owner-occupancy levels above the 20-percent threshold that defines a homeownership desert. As of 2023, the Gateway Cities altogether require a minimum of 10,000 new ownership units to eliminate homeownership deserts (Figure SA-6). Places with the largest ownership gaps include Worcester, which would need nearly 2,500 additional ownership units to reach 20 percent owner-occupancy in each census tract, followed by Springfield (1,300) and Lawrence (1,100). Adjusted for the size of the housing stock, the need is more evenly distributed, ranging from 198 per 1,000 units in Malden to 114 per 1,000 units in Quincy (Figure SA-7). It is important to note that these figures are a conservative baseline: Since 2023, most Gateway Cities have continued to add rental housing, which expands the denominator and pushes the ownership target even higher.

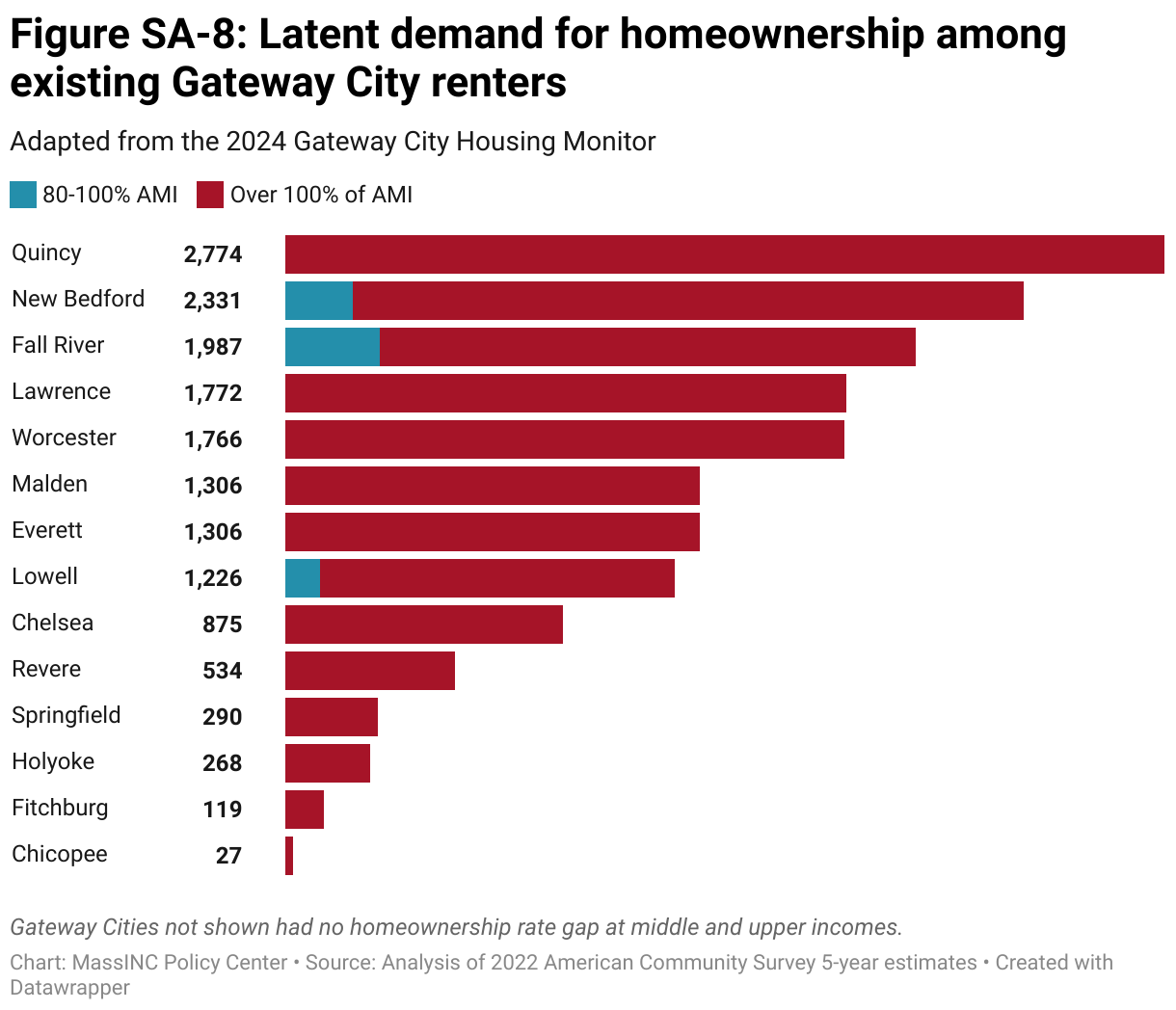

Comparing the number of for-sale units needed to eliminate homeownership deserts with estimates of each city’s latent demand (the unmet internal demand) for ownership shows which Gateway Cities could fill new units with existing residents, and which Gateway Cities would likely need to attract new households. In the 2024 Housing Monitor, we estimated that there is unmet internal demand for roughly 600 units affordable to households earning 80 to 100 percent of AMI and about 16,000 units affordable to those above 100 percent of AMI. However, this demand is not proportional to the additional homeownership needed to address homeownership deserts, meaning that some Gateway Cities have ample internal demand, while others face shortfalls (Figure SA-8). Chelsea, Fall River, Lawrence, Lowell, Malden, New Bedford, and Quincy all have sufficient internal demand to fill additional for-sale units. In contrast, Brockton, Fitchburg, Haverhill, Holyoke, Lynn, Pittsfield, Springfield, and Worcester would likely need to attract new residents to meet their targets, or pursue strategies that expand the pool of potential buyers—such as supporting lower-income households in achieving homeownership or increasing overall homeownership rates above historic levels (Figure SA-9).

The Barriers to Developing More For-Sale Units

To achieve their ambitions for homeownership production, Gateway City leaders and housers must overcome significant barriers to producing ownership units that go beyond the usual challenges of housing development. These barriers fall into two broad categories: a long post-recession hangover that left ownership funding channels underdeveloped and a tenure bias in multifamily development that makes ownership harder to deliver than rental. Insights from interviews with developers, planners, and community organizations help illustrate how these forces interact to shape what actually gets built.

A Long Post-Recession Hangover: The Funding Imbalance Since 2008

Massachusetts is still working to recover from the disruption of the foreclosure crisis, which reshaped its housing finance system and set in motion more than a decade of institutional inertia. Before 2008, the state ran both rental and homeownership funding rounds, with a rough 75/25 split in resources. After the crash, officials concluded there was no market for new for-sale units, and from 2008 until roughly 2019 the commonwealth provided virtually no consistent subsidy for affordable homeownership production.19 Developers and lenders lost capacity in the process: Community-based groups shifted away from producing ownership units, banks grew more reluctant to finance them, and flexible streams such as the Affordable Housing Trust Fund and HOME were redirected almost entirely toward rental.

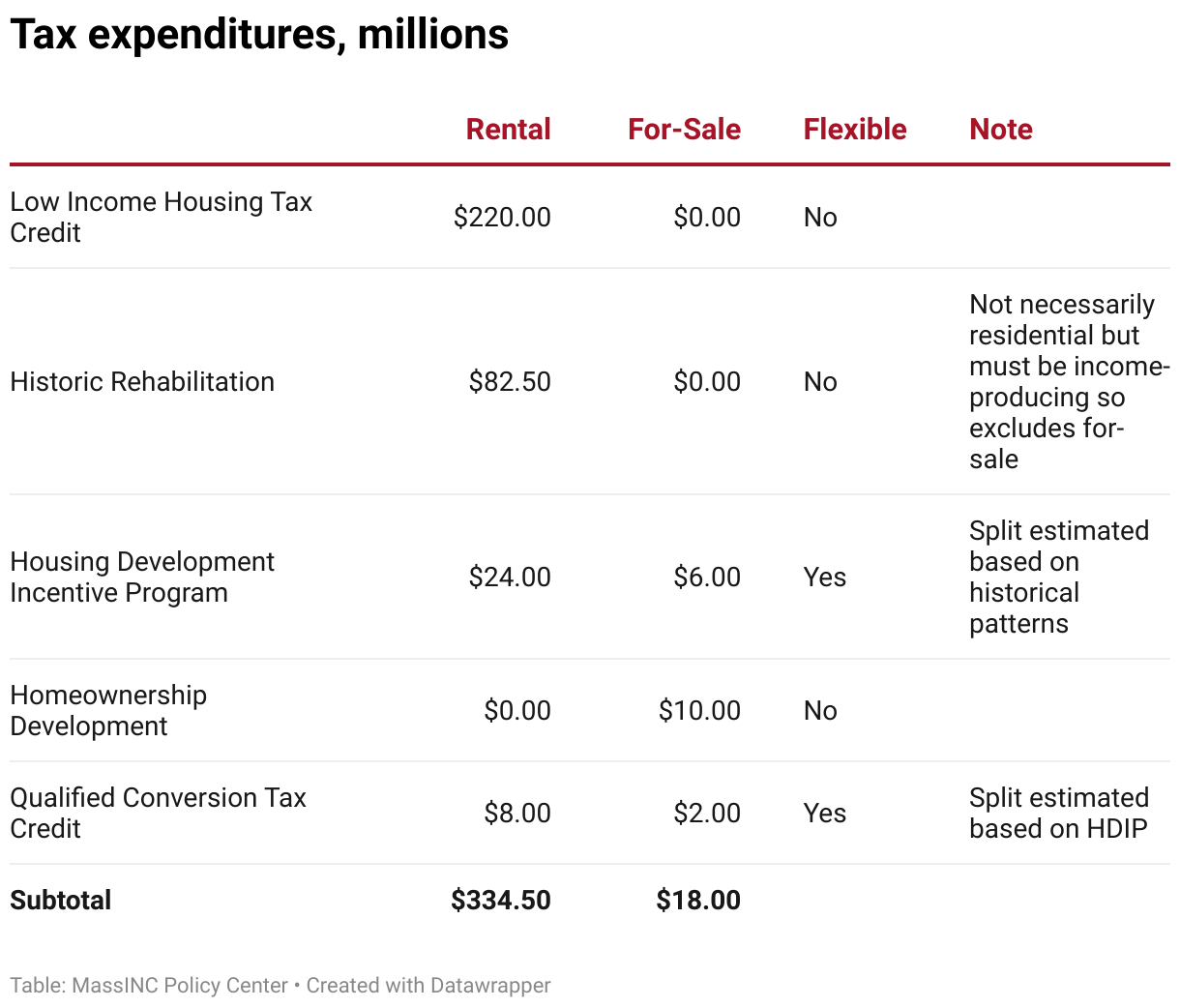

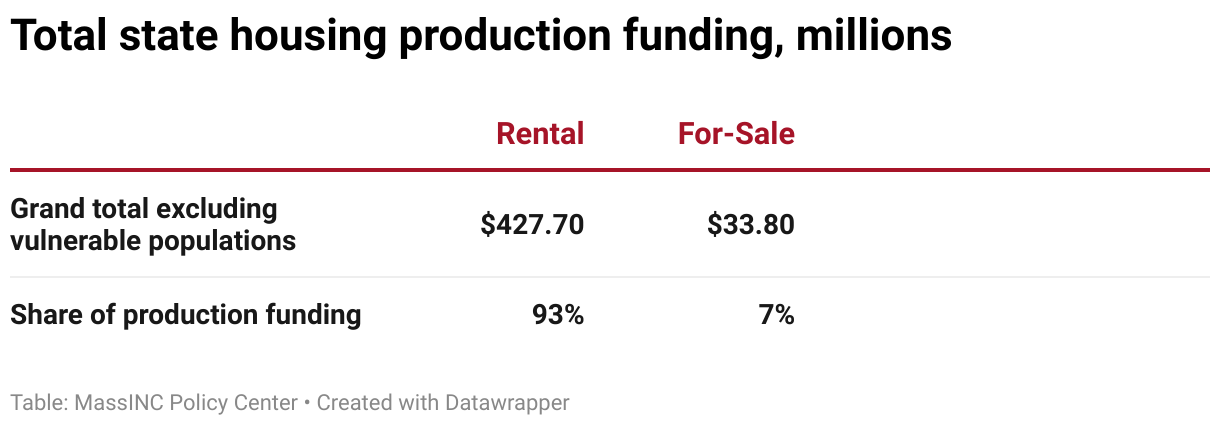

That tilt has proved sticky. In the Healey-Driscoll Administration’s FY2026 Capital Investment Plan, $93 million (excluding programs for vulnerable populations) is allocated to rental development, while just $16 million is allocated to for-sale development. On the tax credit side, the imbalance is even sharper: $335 million in rental credits versus $18 million for homeownership. Taken together, rental accounts for roughly 93 percent of state housing production support, with just 7 percent left for homeownership development. The imbalance is even more severe on the federal side, where most of the supply-side subsidies flow to rental through the Low-Income Housing Tax Credit (LIHTC) program. Massachusetts receives about $200 million in federal 9% credits and another $30 million in 4% credits, which are almost exclusively used for new rental production as well as preservation.20 Adding just the federal 9% credits to the ledger shifts the state’s tenure ratio from 93/7 to 95/5.

The first major effort to correct this imbalance came in 2019, when Governor Charlie Baker launched the Commonwealth Builder program. Designed explicitly to serve Gateway Cities and close the racial wealth gap, it marked the largest infusion of homeownership resources since before the foreclosure crisis. Between FY2021 and FY2025, MassHousing reports committing more than $188 million to Commonwealth Builder projects. The 2024 Affordable Homes Act has since added new tools, including a Homeownership Production Tax Credit and a Qualified Conversion Credit, but these programs will need to be tested and scaled before they can move the needle. Meanwhile, support for Commonwealth Builder has declined—from $60 million at its launch to just $8 million today—even as rental subsidies continue to grow. State LIHTC has expanded from $200 million to $300 million annually, and federal 9% credits from roughly $205 million to $230 million.

Correcting this imbalance will require more than new programs. It demands rethinking the policy and economic ecosystem that has tilted production toward rental—a legacy of the post-2008 shift that has yet to be rebalanced.

FY2026 State Budget for Housing Production

Spotlight: Worcester Common Ground builds affordable homes through creative partnerships

Worcester Common Ground (WCG) works in three formerly redlined census tracts where homeownership is below 10 percent and poverty and resident turnover are high. In this context, the organization has delivered 34 properties with affordable homeownership, from owner-occupied triple-deckers with rental units to single-family homes and duplexes. Producing these smaller-scale projects has grown harder as state programs increasingly favor large developments and as federal compliance costs rise. The Neighborhood Stabilization Program remains one of the few state tools WCG can make use of, and for the first time the group has also tapped Worcester’s Affordable Housing Trust Fund. To keep building, WCG has relied on creative partnerships: a revolving line of credit from UMass Memorial for rapid land acquisition, donated materials from Saint-Gobain, labor from YouthBuild, and support from faith groups such as the Unitarian Universalist Church of Worcester and the Episcopal Church of Western MA, alongside private donors who believe in this work. Each home is placed in a community land trust, ensuring long-term affordability while still allowing residents to build equity; early resales show that families can earn a meaningful return even within their affordability framework.

The Tenure Bias in Urban Multifamily Infill

In Massachusetts’s policy documents, “multifamily” is often shorthand for “rental.” The state’s dominant financing tools reinforce this association: The Low-Income Housing Tax Credit can only be used for rental, and the Historic Rehabilitation Tax Credit is restricted to income-producing properties, steering mill and factory conversions toward apartments. Over time, developers, lenders, and public programs adapted to these rules, building institutional muscle memory for rental pro formas, while losing fluency in ownership models. On infill or large-building sites in Gateway Cities, the default deal structure is rental—not because communities oppose ownership, but because the financial and legal path is clearer.

Other barriers reinforce this tendency. Utility connection fees can be higher if each unit requires its own service. Flood insurance can be required for every unit, regardless of elevation, while there are more flexible insurance policies on the rental side. Bedroom-based parking minimums further tilt incentives toward rental, because for-sale units tend to have more bedrooms than apartments. Small and midsize infill can be particularly difficult. Condominiums have fixed costs such as reserve requirements that weigh heavily on small and midsize projects, but are more manageable when there are more units to spread expenses across.

But the fact that current incentive structures tilt the field does not mean ownership is out of play. Massachusetts law already enables a range of multifamily ownership forms—cooperatives, fee-simple townhomes, and traditional condominiums. The challenge is one of education and experimentation: Policymakers, lenders, and communities need more exposure to these models, a better understanding of their pros and cons, and clearer examples of how they work in practice, so that rules and incentive structures can be optimized to enable more multifamily for-sale production. For Gateway Cities with tight land and aging buildings, normalizing these ownership structures could help expand pathways into ownership and rebalance housing options.

4. Recommendations

Our analysis and interviews with key informants point to several promising strategies for expanding homeownership in Gateway Cities.

- Aim to at least restore the 75/25 division of state housing dollars between rental and homeownership. Before the foreclosure crisis, Massachusetts directed roughly one-quarter of its housing dollars to homeownership production. Today, just 7 percent goes toward for-sale units, even as federal funding flows overwhelmingly to rental. To correct this imbalance, the Commonwealth should aim to at least return to a 75/25 split, with additional investment initially targeted toward programs that already show more demand than funding capacity. The timing is favorable: Beginning in 2025, federal changes to the 4% LIHTC will free up bond capacity by lowering the required match. If Massachusetts takes advantage of this change, it can continue to fund vital preservation projects while using fewer state bond funds for these recapitalizations.

- Target the Homeownership Development Tax Credit to areas with low homeownership rates. The Commonwealth is in the process of deciding how to structure its new Homeownership Development Tax Credit. It could have the greatest impact if targeted to areas with below-average homeownership rates. Beyond promoting more balanced tenure, this approach would also encourage pairing the credit with Opportunity Zone investments, redirecting investor incentives in places where profit motives alone might otherwise reinforce rental dominance. To preserve long-term affordability, however, the credit should be avoided in flood-prone areas where high insurance costs can destabilize ownership.

- Help developers and lenders gain experience with multifamily homeownership models in Gateway City markets. Massachusetts law enables a range of multifamily ownership forms—including cooperatives, fee-simple townhomes, and condominiums—but developers and lenders often lack experience with these models in Gateway City markets. A focused capacity-building initiative could demystify these structures through training for developers, lenders, and local officials, creating a pipeline of replicable projects. Progress will also require experimentation and iterative learning. Pilot projects can surface practical challenges and opportunities, while feedback loops between practitioners and policymakers ensure lessons inform future rules and incentives.

To reduce risk, the Commonwealth should allow flexibility—such as temporary rental conversion or rent-to-own arrangements—if units do not sell. Finally, research on market dynamics—for example, the price premium households place on single-family detached homes compared to multifamily units—would help calibrate incentives and set realistic expectations for uptake. - Explore the use of down payment assistance as an incentive to spur production. Redirecting subsidies from the construction side to the point of purchase can lower compliance costs, while still ensuring affordability. This approach broadens the policy toolbox, blending the benefits of supply-side and demand-side strategies: Developers still deliver new affordable units, while buyers receive immediate equity and lower mortgage costs so they can afford them. However, builders must have the capacity to carry project costs until sale, which can be prohibitive for smaller nonprofits or emerging developers. To make the approach more widely accessible, it should be paired with mechanisms like bridge financing, loan guarantees, or revolving funds, which may require retooling to work in this context.

- Help renters become homeowners in their own communities. Programs designed to improve affordability should also make it possible for Gateway City renters to transition into ownership where they already live. In practice, past efforts such as the Homeownership Opportunity Program often had greater uptake in suburban markets, giving city residents pathways out of their neighborhoods rather than options to buy into them. Similarly, AMI-based eligibility rules for low-cost mortgages can unintentionally reinforce out-migration of higher earners. Unless programs are explicitly structured to counter these tendencies, the natural pull of market dynamics and path dependency will continue to steer resources toward places with higher incomes and higher homeownership rates.

To change this trajectory, supply- and demand-side strategies must work in tandem. Massachusetts needs both an expanded supply of ownership opportunities in neighborhoods with low homeownership rates and demand-side supports that are tailored to help existing renters become mortgage-ready. When aligned, these tools can ensure that revitalization strengthens communities. On the supply side, hybrid models that blur the line between renting and owning—such as rent-to-own or shared equity—can create footholds in the housing market. On the demand side, targeted supports like matched savings programs, employer-assisted housing benefits, credit counseling, and rent-reporting initiatives can help households become mortgage-ready, turning affordability efforts into lasting community gains. - Convene housing leaders to further develop these ideas and forge a cohesive supply-side homeownership strategy for the commonwealth. Building an equitable and efficient homeownership strategy is a complex task. But Massachusetts has a deep well of experience to draw from, and housing leaders have come together previously to sort through these difficult issues and build consensus on different approaches that will work for different communities. The Healey-Driscoll Administration has already demonstrated its exceptional capacity to rapidly develop and implement housing policies and programs to meet acute needs. If the administration applies this same focus and attention to homeownership, there is no doubt that it can position Gateway Cities to build stronger neighborhoods of opportunity.

Spotlight: Deep Down-Payment Assistance in Fitchburg and Leominster

The cities of Fitchburg and Leominster partnered with Habitat for Humanity North Central Massachusetts to pilot the use of deep down-payment assistance as a production incentive. Rather than using federal HOME funds to finance construction directly, the cities directed these funds to serve as down payment assistance for buyers at closing. This enabled Habitat to sell new homes affordably, while substantially reducing onerous compliance costs. The model retains all the benefits of both production subsidies and traditional down –payment assistance—closing the financial gap to make new units affordable, lowering mortgage costs, and providing immediate equity—while reducing administrative burden for the developer. For Habitat, this approach proved both feasible and highly efficient.

Appendix: Defining a Homeownership Desert

Definition: A homeownership desert is a census tract where fewer than 20 percent of housing units are owner-occupied or listed for sale, even after accounting for statistical uncertainty. In other words, it is a place so dominated by rentals that the upper bound of the Census Bureau margin of error still leaves ownership opportunities below one in five homes.21

The technical foundation for this concept draws on the Joint Center for Housing Studies’ 2024 work on rental deserts.22 JCHS set a 20-percent threshold to identify rental deserts because it falls roughly 15 percentage points below the national rentership rate and is lower than in any of the 100 largest metropolitan areas. JCHS further distinguishes between mixed-tenure neighborhoods (20 to 80 percent rental) and high-rental neighborhoods (80 percent or more). Therefore, applying the same 20-percent cutoff to ownership rates highlights places where tenure imbalance is most acute on the ownership side.

In the interest of methodological consistency, we evaluated whether a 20-percent owner-occupancy rate is a reasonable threshold for identifying homeownership deserts in Massachusetts. The evidence suggests that it is. First, 20 percent falls in the bottom 10 percent of tracts statewide, meaning that more than 90 percent of tracts have higher homeownership rates. Second, this threshold aligns with socioeconomic outcomes: Below a 20-percent owner-occupancy rate, the median poverty rate surpasses 20 percent. This 20-percent poverty level is a widely recognized benchmark in federal policy, including regulations set by the US Department of Housing and Urban Development, which classifies such tracts as “high-poverty” neighborhoods warranting special attention and investment.

- Rapoza, Elise and Ben Forman. 2024 Gateway City Housing Monitor. (Boston, MA: MassINC, 2024). ↩︎

- Rapoza, Elise and Ben Forman. 2024 Gateway City Housing Monitor. (Boston, MA: MassINC, 2024). ↩︎

- Rapoza, Elise and Ben Forman. 2024 Gateway City Housing Monitor. (Boston, MA: MassINC, 2024). ↩︎

- Raj Chetty and others. “Where is the Land of Opportunity? The Geography of Intergenerational Mobility in the United States.” The Quarterly Journal of Economics, 2014. ↩︎

- Ann Owens. “Building Inequality: Housing Segregation and Income Segregation.” Sociological Science (2019). ↩︎

- Michael Schill and Susan Wachter. “Housing Market Constraints and Spatial Stratification by Income and Race.” Housing Policy Debate (1995). ↩︎

- Kim Manturuk and others. “Perception vs. reality: The relationship between low-income homeownership, perceived financial stress, and financial hardship.” Social Science Research (2012). ↩︎

- Eric Hanushek and others. “Disruption Versus Tiebout Improvements: The Costs and Benefits of Switching Schools.” Journal of Public Economics (2004). ↩︎

- Denise DiPasquale and Ed Glaeser. “Incentives and Social Capital: Are Homeowners Better Citizens?” Journal of Urban Economics (1999). ↩︎

- Marjorie Kelly and Sarah McKinley, Cities Building Community Wealth. The Democracy Collaborative, 2015; Esteban Rossi-Hansberg and others. “Housing Externalities.” Journal of Political Economy (2010). ↩︎

- For-sale units could be included in HOPE VI and Choice Neighborhoods housing projects, but program funds were primarily directed toward rental redevelopment. ↩︎

- Lyndal Bond and others. “Mixed Messages about Mixed Tenure: Do Reviews Tell the Real Story?” Housing Studies (2010). ↩︎

- Rhett Morris and Rohit Acharya. “Reducing poverty without community displacement: Indicators of inclusive prosperity in U.S. neighborhoods.” (Washington, DC: Brookings Institution, 2022). ↩︎

- City of Brockton. A Blueprint for Brockton: Final Comprehensive Master Plan, 2017. ↩︎

- City of Fitchburg Annual Action Plan (HUD consolidated plan), 2025. ↩︎

- City of Lowell. “Lowell Homes and Housing: Housing Production Plan.” Lowell Forward, 2024. ↩︎

- City of Springfield, 2025-2029 HUD Consolidated Plan. ↩︎

- City of Worcester. Worcester Housing Production Plan, 2025. ↩︎

- The one exception was a funding round in 2014 providing $9 million in state funding for five affordable homeownership developments. ↩︎

- See: https://willbrownsberger.com/federal-low-income-housing-tax-credit/. ↩︎

- Only census tracts with at least 200 housing units were evaluated. ↩︎

- Whitney Airgood-Obrycki and others. “Rental Deserts, Segregation, and Zoning.” (Cambridge, MA: Joint Center for Housing Studies, Harvard University, 2024). ↩︎

2025 Gateway Cities Housing Monitor

Chapters

2025 Gateway Cities Housing Monitor

September 17, 2025